The other day one of my main ladies mentioned how she would like to get a nose job. I was a little confused, as nothing seems inherently wrong with her beak. Sure, it’s more prominent and longer than say, a field mouse’s, but there the striking aspects end. Nothing crooked or aggressively hooked about it, nor wide and illustrious as a joyful potato. Just present, as is tradition.

My initial response was to tell her not to worry. “Your nose is fine, so why change it?”

“Because some people make fun of me.”

Some. Hardly worth redirecting your life and spending $10,000 on the rhino express over, right? I mean, it’s a vanity project directed at other characters, and less so personal happiness.

That’s a wrap, I suppose, of the Hallmark variety. Written and produced by George Santos.

Still, I can’t help but wonder where my own motivations might be sourced. Am I advising her against it strictly because plastic surgery is unnecessary for anything other than severe disfigurement? Do I genuinely reject the vanity polishing popular in our looks-fixated world of Black Pill deniers? Is it some Quixotic mission to boost the fragile female ego in a nice guy’s fashion?

Possibly. On the alternative front, perhaps my schemes are less pure. If she gets the rhino procedure, her looks may indeed be enhanced, thus drawing more attention (and competition) into the mix. I might inadvertently lose something of value by not beseeching an endorsement of the contented pose. Visible elevation could absolutely better her experiences and prospects in life, hence my ulterior motive rises to discourage the surgery, only in supportive and self-righteous terms.

About a week ago some cable network marionettes carted out a few professors to provide “robust analysis” on the new presidential rankings list. To nobody’s surprise, the top spots included figures like George Washington, Abe Lincoln, FDR, and Teddy Roosevelt. At the bottom (counting up), we have James Buchanan, Andrew Johnson, Franklin Pierce, and of course Donald Trump. Hilariously, William Henry Harrison, who occupied the White House for a few months before passing away, was ranked higher than Donald, along with Millard Fillmore and Warren G. Harding. The experts proceeded to note that Andrew Jackson lost ground in the rankings, speculating that this was on account of Trump being a fan of Old Hickory. Finally, the empowered and oppressed female professor expressed dismay that slave-holding presidents would still rank high on the list.

Leaving aside the amusing dynamics of FDR being in the top five immediately after the “Stop Asian hate” campaign, and Teddy Roosevelt, who complained about “race suicide,” I was struck by the shallowness of it all. These are after all learned individuals with countless papers, books, and at least one dissertation under their belts, yet the behavior is unchanged. Still we can expect the aggressive public shilling for mainstream narratives, regardless of their cost to history and truth. Anything to avoid getting targeted by a rage pill mob, I suppose.

The broader problem of “listen to the experts” was highlighted by the U.S. experience with COVID-19. As we all know, the government’s response was a hodgepodge of finger-pointing, political hedging, and flat-out delusion. When lockdowns were first proposed, no one could agree with a broad strategy, leading to a patchwork quilt response by the so-called intellectual class. A most vivid instance of this disconnect came when health experts condemned protestors who opposed the lockdowns while shortly thereafter approving demonstrations against police practices. Were the eggheads really motivated by research, or a profound desire to not be tarred and feathered on social media for their consistency?

This raises a bigger question about who one can trust to give good advice. If doctors are “afraid of the backlash” caused by advising against say, the annual flu vaccine, then how can they be relied upon to make proper calls in other areas? As far as many of us know, the man in the white coat could be prescribing indirect poison simply to keep his public image intact. It’s a total minefield, yet even bringing up the issue smarts of being a heretic under the religious purges of olden times. Difference is, they didn’t have social media and Google reputations to worry about.

I suppose it renders my soapbox rather past expiration, but I have to stress the importance of performing due diligence in all aspects of life affecting your health, emotional well-being, and finances. I don’t care if the speaker has a PhD, or indeed rails against higher education every single day to get views. The moment you permit your mind to be outsourced is the start of a long (and potentially hazardous) decline. Steel your brains, and look past the welcoming glow. Experts or not, they’re only human.

In real life, which is sometimes less believable than the internet, I tend to dispense with formalities and grandiose declarations. If I have a goal, it gets written on a scrap of paper, which will ultimately be shredded or burnt, because the vehicle itself is unimportant. What matters is my personal drive to complete the requisite objective, not how ceremoniously it was announced. This may be the fault of seeing far too many people over the years making bombastic commitments about changing their lives, only to abandon the cause after life gets in the way. Nevertheless, it works.

Except this year is different. No, I still refuse to outline some progressive scheme of self-betterment which can hopefully satisfy the local bar’s social circle long enough to sound relevant. The thought of such a process remains toxic to my senses. Instead, I am determined to continue forging a path based more on empathy for others. It is almost certain that the word elicits a clichéd eye roll from readers, yet I advise taking a pause. What I mean by empathy is challenging oneself to sincerely understand the position and life experiences of others, as opposed to either dismissing outright or mindlessly groveling before their interests.

The mere prospect of this path does not come easy to me. As a child, I concluded early on that the world had no respect for exhibitions of emotion or vulnerability, particularly from a man. Even the souls who claimed to have sympathy for such expressions would be quick to document and use them against others, typically in pursuit of personal aggrandizement. Tearing up as a boy was social suicide, just like recognizing the innate injustice of a system made you a pathetic victim. A superior approach meant being unmoved, resolute, and condescending, all traits of the “real” man.

Satisfying as these proclivities might be in the short-term, they are immensely destructive when applied across the span of life, and even more so in society. Resorting to hazing and mockery of others serves to mask genuine corruption infecting a system, whether between individuals or behind an organization’s doors. Complaining about a serious problem like manipulation or even abuse becomes the basis for a counterattack which labels the honest observer as a poisonous barnacle likely to destroy the ship. “Shut up and do what you’re told” begins to prevail, and anything else tastes of crime.

On a macro level, the mentality of refusing to comprehend other outlooks produces disastrous outcomes in national policy. Some years back, I would have giddily jumped on the bandwagon to condemn welfare users without even considering their individual status or backgrounds, which are less disdainful than many would believe. I did so because to defend them would indicate weakness or laziness, both threats to the meritocratic order we all subconsciously adhere to. Providing those people were a blurry monolith of greed offered up by shock jocks and politicians, they were incredibly easy to write-off as entirely worthless from a social standpoint.

We can see a similar dynamic inherent to issues like migration. Liberals clamor for acceptance of higher numbers in the name of human rights or decency, while seldom stopping to seriously consider how their own consumerist habits and social polices destroy traditional communities once operating on subsistence practices, if with less progressiveness than the leftist desires. Conservatives on the opposite agitate for walls and moratoriums, while also ignoring the unpleasant facts of U.S. involvement in destabilizing southern countries through the drug war and anti-leftist warfare. Unfortunately, the way we go about swiftly cordoning and demonizing rational analysis of any situation allows these illogical placeholders to not only remain, but grow stronger than before. Fighting back requires an open mind, something hardly valued in the days of now.

Much as I may not have control over the world, nothing prevents me from demanding higher personal standards in this regard. Thus my continuing mission for 2021 will be to examine more of what I disagree with, and strive to at least know where and why others have formulated their own biases or grievances, even if my initial reaction would normally be to wave them off. It stands to be a fascinating adventure.

When we are young, viewpoints tend to be informed but whatever structure or experience is immediately surrounding us. This might include features such as religion, class level, familial structure, or household setting. Over time we (hopefully) get the chance to expand our sphere of understanding through education and the pursuit of association with a wide variety of experiences which can serve to dislodge or strengthen prior opinions, depending on the impact. Ideally, the typical person will evolve gradually into a well-rounded individual with personal drive for learning and the humility to continue growing throughout life.

That is, ideally. In the torrid reality of our existence, few people bother venturing past the “Drop Off,” where they might actually face challenges to long-held opinions. Instead, what has been known and accepted for years is simply reinforced, not forcibly through validating scenarios, but a general inability to scrap together the time needed for such change to occur. Busyness, or the impression thereof, simply lays the foundation of contended indifference towards the unknown frontier.

As noted before, this severe shortage of hours (or lack of access) can prove radically dehabilitating to the anxious mind. Millennials are the first generation to have steady means of getting on the Internet dot com, yet even there the pockets of time available for superficial research – let alone critical reading—are minor between work and digital socialization routines. One almost has to demand the blocked out portion of a given day or weekend to ensure it occurs, and even in that case the guarantee falls less than confidently.

Now, should the research get started in earnest, the relative speed of accrual can still present a bedeviling reality for curious learners. Books take time to finish if they are going to be covered concretely, and certainly note-taking can extend this process. Then there is the question of which others to read, and the specific order of tackling, plus the overall reliability of the authors. Things can swiftly become a minefield of careful assessment and budgeting to determine precisely what writers are worthy of attention, or the most generic respect.

Perhaps more crucially, the aforementioned debate over order could serve to delay access of an important source. Taking the example of dieting books, if a person avoids reading a particular title for one or two years due to time constraints, they are likely to have gone that entire period potentially eating foods that are unhelpful to bodily prosperity. There is no basis to indict their ignorance, as it remains unwilling, yet the long-term consequences stay grim. Thus we are all victims of what we do not yet know, and may never until it is too late.

A visible phenomenon I’ve witnessed over years as an online personality is the general peevishness shown by younger people towards any information on the internet with a price tag. They have no problem adding stuff to the cart on mom’s Prime subscription, but once outside the safe zone of parental compensation, everything seems too expensive. Not only that, but the very act of placing an item for sale is responded to with derision and outrage, as if the seller has some nefarious or insincere motivation behind their storefront.

It’s worth chasing an explanation of just why this behavior occurs. To start, we must recognize that few present partakers had any role in the creation of the internet machine, and even less possessed the intellectual capacity to even conceptualize it before Internet Explorer was the bomb. Those higher IQ folks who did join the party managed to create a fairly-accessible model, bound up in their idealism and general libertarian philosophy. They obviously monetized the juggernaut with advertisements, but as far as regular browsing and access, one doesn’t pay per page, or per download, save through subscription to a service provider.

Consequently, young people have been brought up with the idea that all content is free, unless of course they wish to donate to a pair of yoga pants on OnlyFans. Millions of hours on YouTube, an open access encyclopedia, and free educational services make youthful souls believe only their own mindset is a limitation, not money or credit. So naturally the moment a person attempts (even if they didn’t) to generate some return on their offerings, the digital liberty peepers are back to screech about “grifting,” or “taking advantage of us.”

The former claim strikes as rather odd, because such behavior seems more attune with a person asking for donations which are unneeded, or using corruption in government to profit. On the flip side, presenting some products for purchase at low price tags, with the option to return digital options within a week for refund, hardly falls into the same category. If anything, it simply displays a reality containing the sacrifices of life, particularly when hours are poured into a single work. Gaining a modest (and often negligible) return from that effort is the principle, one that many of course reject outright. As for the secondary possibility, no one is forced to buy, yet they still grumble.

Part of the issue might relate to differences between creatives and consumers. The first squad understands the struggles of late nights, edits, curriculum-building, research, and design. They have lived the casualty time now lying as distant memory, and wish to recuperate a sliver of what’s lost, more in honor of those hours spent than for financial reasons. Our latter friends simply view the finalized piece and hide behind their glistened frustration that someone might make money, or is simply daring to do so. “It should be free,” becomes their long-standing cry, as castigation for merchants with the gall to become better rise upon lips.

At the end of the day, the entitlement mentality will only worsen if jobs become scarce in the future. Deprived of money – or at least more than a pittance – the Zoomer-tier Moolenials shall rain spiritual anger down upon the independent content creator, banishing him to parts unknown, where attention is little and peace of mind abundant. Then the angry freedom fellow will mozy on to Amazon, and add some more items to his mom’s cart, perhaps now funded by that seductive Freedom Dividend.

Sometime back I produced a video concerning the problems entailed by our dalliance with modernity and technological progress. My penultimate suggestion was for people to re-embrace nature, opting for smaller communities with solid values over the cosmopolitan sprawl, or farms instead of NYC apartments. In response, lurid and sarcastic replies bubbled up from the happy Ethernet cords wrapped around the electric maze of the world. They smugly advised, “Practice what you preach,” the comfortable retort that allows irritated lumps to quickly resettle into the brain-destroying digital resort without feeling a call to change.

For the record, I have already made leaps and bounds in the “less-grid” direction. I own a decent plot of land with two well systems, a garden, and a large walnut tree. Composting is a regular practice, and I am gradually shedding processed foods from the dietary plane, in many cases creating consumables from scratch. My skills with crafting clothes by hand are not immaculate, but they improve on the regular.

None of those disclaimers should matter insofar as the thrust of history is concerned, however. Recent reports, which are only surprising to the uninformed and socialist, suggest Wall Street is now delving into futures contracts involving water. The development has tickled many concerned senses because of projected water shortages, with two-thirds of the planet’s population expected to face supply issues by 2025, with many already experiencing the unpleasantness.

Enlightened folks have seen this coming for years. The incessant push for growth, for globalization and free movement of peoples, all in the name of economic profit, can lead but in one direction. As basic natural resources shrink and the gluttonous thirst to build more continues unabated, there will be further attempts to buy up valuable land and lord it over the poorest of creatures. Even the homeless squatter in the woods may find himself litigated out of existence so some sycophantic corporation can expand its quarterly earnings report. The dreaded sludge seeps on.

What can any lone man do? Resist with lifestyle choices. Take your wallet and carefully consider where to settle, hopefully escaping the pollution and scum-populated urban areas for distant peace. If funds are not available for a house, buy the land itself, preferably with access to fresh water. Get a camper or a van to start with. Look into solar and gravity-powered technologies. Learn to cook. Respect natural systems and work to preserve them. Read so you understand the problem.

As for investment options, look into Xylem and PIO as starting points, along with others. The former has experienced a decent run, and I’ve witnessed its penetration on a local basis too. PIO thus far hasn’t wowed anyone, but that could change. Watch out for that pricey expense ratio, which currently clocks in around 0.75%.

More than anything, be prepared to swim, even if you dance amid the sands of a dry wasteland.

The clear and present normal to see on the Twitter pages of the young and upcoming is a statement reading something like “My opinions are my own.” Try as I rack the brain, it is difficult to comprehend the logic behind such a statement. Sure, the world is fond of disclaimers, a dynamic which probably helps account for the lawyer-loving culture we live in, and the lawsuits that go in unison. But does it really matter?

Suppose the empowered tweeter does feature said tagline, and puts out a joke that sounded good in his head, along with everyone else’s not sworn to petty drama. Will this really protect him from consequences? Perhaps the company he works for is off the hook, but should something come to the level of defamation, good luck with that. The banhammer is coming for job, reputation, and dating patterns, determined to drive that poor soul into the grounds of repentance—although don’t expect mea culpas to change anything.

Saying your opinions are your own is like cushioning unpleasant crime statistics by noting “I’m not a racist.” Even issuing such words is enough to indict, “facts and logic” aside. The very lifeblood of modern drama culture is oriented around picking out some semantic weak point or bad take and attempting to ruin the person’s life over it. Accuracy and disclaimers be cursed, so let them pay reparations and shut up.

The result is that such folks end up muzzling themselves to degrees not previously believable. It is hardly enough to tow moderate individual opinions; now you are expected to ferociously endorse the party line, regardless of how hypocritical and corrupt it happens to be. The religion of the stato-multinational establishment demands nothing less, and traitors pay the hearty price. One cannot merely be a passive associate; they must embrace the cause of passionate cultist and acolyte.

It would seem as though a simpler solution can be had: speak your mind, but under a different name. Few things enrage the village idiot cancelist more than not being able to perform a quick Google search which brings up name, rank, and serial number. No open Facebook page or LinkedIn profile offering information on where, who, and what salary materializes gets their bones cooking, while also staving off the less zealous investigators. You might just keep that paycheck and apartment a little bit longer, providing of course there’s no camera in the details.

Or you can be a politely disclaimed free speech “hero,” and hope for blueberry pancakes with a chance of employment.

Before her death in 2016, the legendary Ursula Le Guin gave a short acceptance speech at the National Book Awards in which she outlined the problems with modern publishing. At that stage of her career, she could safely issue the criticisms without fear of financial repercussion, but the observations were nevertheless poignant. They rest firmly on the role which capitalism can play in diminishing the value of literary art by commoditizing various genres for mass market efficiency. Some particularly biting lines are as follows:

“Hard times are coming, when we’ll be wanting the voices of writers who can see alternatives to how we live now, can see through our fear-stricken society and its obsessive technologies to other ways of being, and even imagine real grounds for hope. We’ll need writers who can remember freedom – poets, visionaries – realists of a larger reality.

Right now, we need writers who know the difference between production of a market commodity and the practice of an art. Developing written material to suit sales strategies in order to maximize corporate profit and advertising revenue is not the same thing as responsible book publishing or authorship.”

One cannot deny the truth in those words. The more that technology advances, the less substance matters, and this can be witnessed across various mediums. A person with great content on YouTube will swiftly get buried by the excess of “corporate friendly” channels letting our dopamine-hungry brains feast on countless jump edits and sound effects. Movies with independent or unique origins are disregarded, while studio money pours into toxic remakes, and the coarse boredom of social justice slinks into genres where it was always present, albeit with class and subtlety.

Books are no exception to this rule. As others have observed, the idealized vehicle for publishing success has become a pantomime of the same writing style and setting, regardless if it lacks originality. Even the famous fantasy series popularized by an unknown homeschooler relied on heavy borrowing from the Star Wars movies, to a degree that is almost comical. But it still sold, because publishers are more interested in what fits the market than anything resembling genuine art. It’s not a stretch to say that Paolini would have been laughed out of the room had his book done something truly beyond the bounds of “comfortable” prose.

Le Guin went on:

“Yet I see sales departments given control over editorial. I see my own publishers, in a silly panic of ignorance and greed, charging public libraries for an e-book six or seven times more than they charge customers. We just saw a profiteer try to punish a publisher for disobedience, and writers threatened by corporate fatwa. And I see a lot of us, the producers, who write the books and make the books, accepting this – letting commodity profiteers sell us like deodorant, and tell us what to publish, what to write.

Books aren’t just commodities; the profit motive is often in conflict with the aims of art. We live in capitalism, its power seems inescapable – but then, so did the divine right of kings. Any human power can be resisted and changed by human beings. Resistance and change often begin in art. Very often in our art, the art of words.“

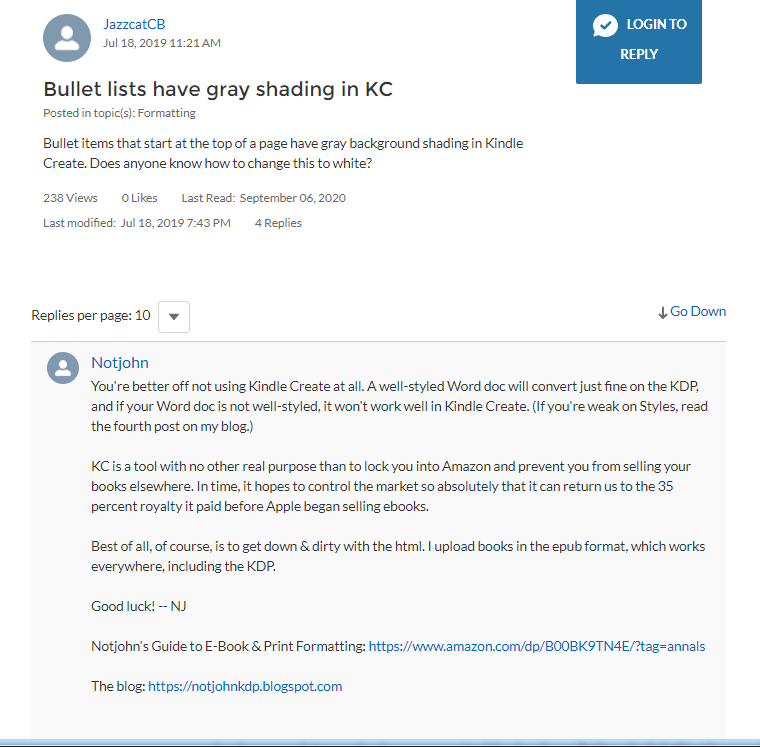

I believe in this case Le Guin was referring to Amazon, and rightly so. The compounding growth of Bezos’ bright-eyed promotion of publishing hides a more sinister reality: Amazon’s attempt to form an effective sales monopoly and reduce current royalty rates. Part of the approach involves encouraging authors to publish with Kindle Create, a clunky and unhelpful software designed to coral authors into the Bezos marketplace indefinitely:

Ultimately, it is hard to say what the future will hold. Perhaps Le Guin is right, and change will arise. For myself, I know that my hesitation in publishing fiction as opposed to non-fiction (and especially self-help), stems from a recognition that the themes depicted in my stories would be swiftly dismissed, if not entirely deleted, from the Amazon platform. But that is the tragedy of being a writer: you can’t help but write, even if the outcome is a pittance. It is an extension of the soul, and not doing so feels tantamount to betrayal of the spirit.

The internet seems profoundly obsessed with individualism. People harp on it to no endless degree, promising the wonderful gifts of “financial independence,” self-determination, and purposeful existence. Others present rather basic ideas as miraculous truths, developing followers who aggressively preach the merits of self, while suspiciously eyeing “collectivism” and its assorted malevolence. If cooperation is so much as suggested, these creatures leap to the defensive plane, accusing their opponents of endorsing socialism, or subverting the dignity of liberty. They rush to protect the individualism tribe, and gain immense satisfaction from such fulfilled duty.

A most apt question here would be: why? Once we peel back the outraged drama and look at actual human behavior, the stark individualism of people is manifested in an exaggerated manner which rises to frustrate the suggestion of our aforementioned friends. If anything, society is far more dedicated to the illustrious self than the promoter wishes to imagine.

Suppose for example one is going to purchase a car. Perhaps they will buy something to impress people in close communion with them, or even take friendly advice on the matter. More often than not however, the decision is driven by personal (read: individual) qualities. It could be a beater model, chosen because that chap can’t afford something on the pricier side, or possibly a vehicle which “matches my personality.” Never mind how those folks typically say they are focused and reliable whilst buying a Chrysler; the point remains as an individualistic contention.

Colleges and living spaces are similarly outlined. If it is financially viable, or happily debt-fueled, highschoolers will typically choose an institution with the appropriate program to match their personal interests, preferably in a state or country with enjoyable backdrops. Sure, the skeptic could argue that most college institutions have a Marxist hive mind, but at least in theory the students are exercising a degree of independence and personal choice. Once they graduate, certain cities might hold appeal for the diversity and nightlife, while others retreat to the country roads. Are these normal patterns of human behavior all reflections of some collectivist conspiracy?

Even the push for FIRE lifestyles on the internet dot com invariably leads to more self-centeredness and LESS focus on the community. The act of budgeting away little things like the morning coffee or diner breakfast to save money diminishes the chances of interacting with others and supporting a local (or chain) business. Another clear and present theme in the financial-digital realm is the emphasis on not having kids in order to retire early. As far as the checkbook side of things is concerned, this makes perfect sense; why would anyone reproduce if the cost of raising one child can be as much as $233,000, not counting college? Yet somehow we are not individualistic enough.

Perhaps the real issue is more complicated. We already are highly individualistic, and well-adapted for a consumer capitalist society, but this is not adequate. Instead of people finding meaning in family and community, which have been stained by the collectivist shackles, they turn to some higher level of individualism for salvation. Just a little more self-improvement, positive mindset-building, and financial freedom. Then I’ll be a REAL individual. So Able Earnest proclaims, as his life becomes emptier by the waking second.

This concept collides with Emile Durkheim’s idea of the anomie, or disconnection of individuals from social standards and economic systems commonplace in advanced societies. It develops as a “malady of the infinite,” where the person in question constantly desires more, but cannot be satisfied in the confines of his social system, leading to derangement or possibly suicide. Likewise, modern neoliberal cultures fixate on meritocracy and individualism, while suppressing the value inherent to Bilbo’s “home above gold” or group solidarity versus individualism.

But I’m just a jealous collectivist, so pay no mind.

A sad casualty of the information age has been the general dumbing down of arguments made by people, especially on the internet dot com In days past, those who were motivated could read and craft arguments from such sources, with few SparkNotes, 5-minute histories, or other shortcuts available. Less-informed folks might mouth off in a tavern debate, but they had to conjure up wild claims without the generous assistance of a search engine. Faking it took some effort, despite the imperfections.

Today we sense a different horizon. Every Jermaine, Reese, and Zephyr can simply pop a question into Google, hit the search button, and copy-paste a hyperlink purporting to back their claims – even if it comes from the likes of Quora, Yahoo Answers, or perhaps “Ask Jeeves,” if the latter even exists. There’s no prerogative to read the actual body text or explore citations, because what supports them MUST be accurate and beyond reproach.

On the surface level this dynamic is not so problematic, yet it renders a larger-than-life proportion of the national population quite confident in their own opinions, no matter how incomplete those thoughts might be. The internet’s affordance of little introspection for their purposes means those fragile links serve to enhance the ego, and assure a diminished likelihood of further investigation of the material. After all, with that argument remanded to the “settled science” cranial bin, what more is needed?

Perhaps a great deal. Unfortunately, the people who bother to distill petty emotions and look at raw information are left victims of fellow internet people and their mindless bloviation. Since the former group tends to be humbler and more patient, discussions typically end with their voice being drowned out by a million smug cries from the effectively illiterate. Ambition to change the norm shatters upon a weathered hill where the shallow brains defecate pure dopamine satisfaction, while always thirsting for more.

In the interest of not becoming one of these said gremlins, it is imperative to be illiberal with the surrender of your mind. Before wading into a debate, pause to consider how thoroughly the concept has been understood. Failing to do so can result in a situation where bluster and invented facts are necessary to remain credible, methods avoidable when adequate preparation is undertaken. Sure, the appeal is significantly less wonderful, but at least time is not wasted by lowering ethical standards merely to survive.

You must be logged in to post a comment.