What the heck is THAT?

We’re talking about the elusive “Expense Ratio,” which governs some of the charges passed on to the investment fund participants by money managers. In most cases, this figure will be something like 0.04-0.99 percent, numbers that successfully flummox the mathematically disinclined. They don’t look expensive, and in fact they really don’t seem like much at all.

But the truth is in the fee lines. If you go by the first glance, it is easy to end up paying hundreds if not thousands of dollars worth of expensive charges that eat away at the base return.

Consider the following S&P 500 options for a second, and keep in mind that the returns are a few months old:

American Funds AMCAP Fund

5-year return: 8.94%

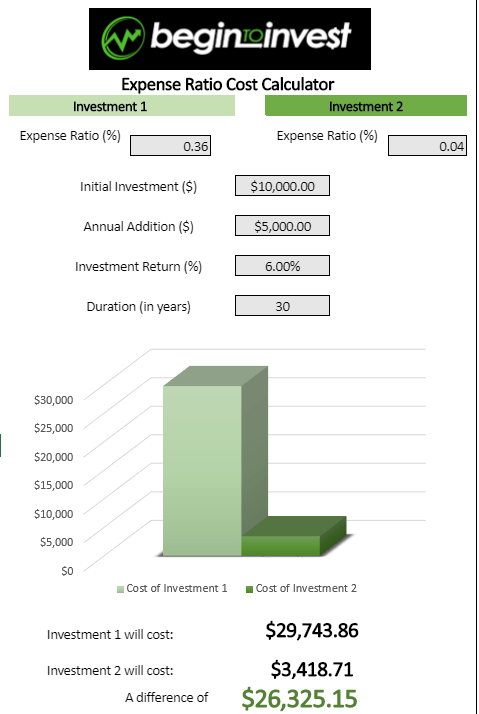

Gross and Net Operating Expenses: 0.36%, or $3.60 per $1000

Vanguard Institutional Index Fund

5-year return: 9.63%

Gross and Net Operating Expenses: 0.04%, or $0.35 per $1000

Those numbers make a BIG difference, and we’re not even including the other administrative fees. Plugging them into a calculator we get:

A difference of over $26,000 over thirty years, all while the participant thought he was “saving” money.

Now let’s look at a bond fund for comparison:

Ivy High Income Fund

5-year return: 3.91%

Gross and Net Operating Expenses: 0.57%, or $5.70 per $1000

What’s really sad is that the bond fund has a much lower return, and yet charges higher fees, eating away at growth for the saver or retiree. Expense ratios DO matter, even if they seem like legalese at first glance. Choose the low-cost fund whenever possible

One thought on “Expense Ratios Simplified”